Published May 25, 2026

16 Digits vs Stablecoin

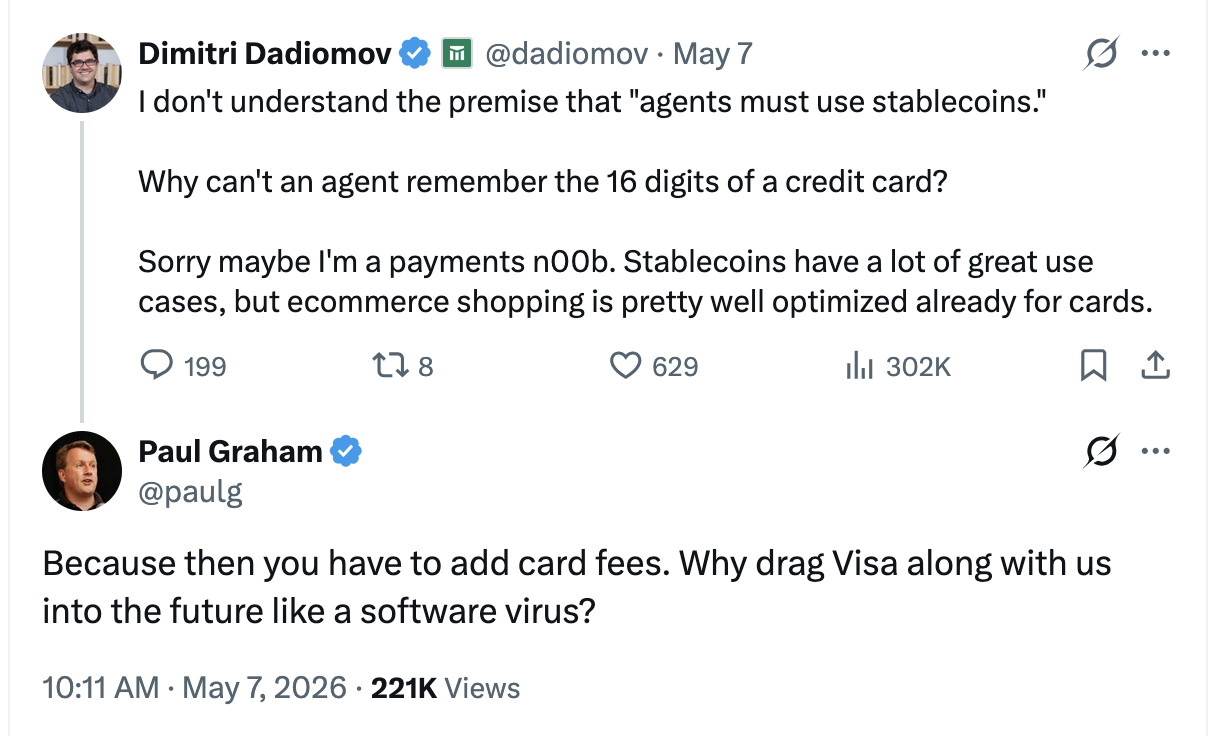

The co-founder of Modern Treasury tweeted asking why we can't just give 16 digit card numbers to agents, because stablecoins are being touted as the more attractive option with the AI boom. Paul Graham responded that it would mean we'd have to pay card fees, and drag the networks into the future with us. At the risk of encouraging Jamie Dimon to buy yet another software company/entity, I wanted to share what I think it would take to make crypto the mainstream choice for payments in the US, and why the networks were successful in achieving it in the first place.

Visa used to be directly embedded inside of the major US Banks. Today, an acquiring bank sends payment details to the network. The network works with the issuing bank to get the funds. All the major characters are banks, except the network. Due to pressure from legislators surrounding this process being siloed inside of a bank and the bank also setting the fees for the merchants, Visa eventually becomes a privately held separate entity and IPOs. The National Automated Clearing House Association in the US that is responsible for governing ACH transactions started as an American Bankers Association owned entity. Today, it is a non-profit. The actual money movements are done by the Federal Reserve and The Clearing House; with the latter being an entity that was also first established by a group of NYC banks.

Stablecoins are a type of cryptocurrency that emerged in 2014 to tie value to a more stable asset like currencies. The most common ones are fiat backed, so that they maintain relative stability, tied to USD, for example. What this means in practice is that the asset is transferred on the blockchain via a cryptocurrency exchange, and then converted into the intended currency. For this work, the blockchain fees, exchange platform fees, withdrawal charges, and provider fees for converting the currencies contribute to the final price.

Do you know the 'how do you do fellow kids' meme, where Steve Buscemi has a red hat and a skateboard? Banks and traditional card networks feel like Steve, while stablecoins are the fellow kids. Walk with me. Despite liquidity concerns, incumbent banks and legislators are embracing stablecoins by integrating them and creating legislation to support them (see Genius Act). I suspect it is related to not being left behind. I think that although stablecoins offer unprecedented speed precisely because they operate outside the traditional banking system, this "outsider" status will deprive them of the structural capital, regulatory cover, and institutional power necessary to reach the mainstream scale of legacy institutions like Visa, Mastercard, or The Clearing House.